By: Ashley Harris, DVM, DABVP– WagWay Chief Veterinary Officer

As a veterinarian and Chief Veterinary Officer at WagWay Group, I’ve seen firsthand how medical costs can impact pet owners’ decisions about their animals’ health. More pet parents, particularly Millennials and Gen Z, are turning to pet insurance as a way to ensure they can provide care without breaking the bank. In this article, I’ll break down the pros and cons of pet insurance, along with research-based insights to help you decide if it’s the right choice for you.

The Growing Popularity of Pet Insurance

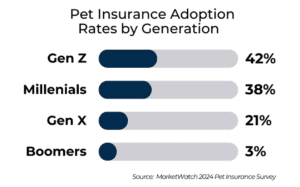

Pet insurance is on the rise in North America. In 2022, $3.2 billion was spent on pet insurance premiums, marking a 24% increase from the previous year, according to the NAPHIA – North American Pet Health Insurance Association. This growth is largely driven by younger pet owners—Gen Z pet parents are 16 times more likely to insure their pets compared to baby boomers.

The surge in demand can largely be attributed to rising veterinary costs. Advances in veterinary technology, specialized treatments, and improved diagnostic tools all come at a price, making the financial burden of pet care significant. Veterinary care expenses have soared in recent years, especially for emergency treatments, surgeries, and chronic condition management. As a result, many pet owners seek insurance to try to manage these potential costs.

But is pet insurance really worth it? Let’s weigh the pros and cons.

The Pros of Pet Health Insurance

- Financial Peace of Mind One of the primary benefits of pet insurance is financial security. Unexpected medical emergencies can cost thousands of dollars. Having coverage allows pet parents to focus on their pet’s health without worrying about how they’ll pay the bill, and their pet’s benefit. Let’s consider the pet parent’s point of view:

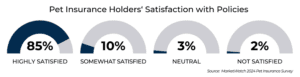

- 85% of pet owners with insurance believe it’s worth it, according to a recent MarketWatch survey.99.5% of policyholders surveyed reported that they do not regret having pet insurance, knowing their pets are covered for significant expenses such as surgeries, diagnostics, and ongoing treatment.

- 99.5% of policyholders surveyed reported that they do not regret having pet insurance, knowing their pets are covered for significant expenses such as surgeries, diagnostics, and ongoing treatment.

- Pet owners without insurance are nearly 1.5 times more likely to avoid the vet and delay needed care compared to those with insurance.

- Coverage for Major Medical Emergencies Most pet insurance plans cover accidents, illnesses, surgeries, and even diagnostic testing. According to NAPHIA, the most common claims include treatments for cancer, allergies, and broken bones. This kind of coverage is especially beneficial for large-breed dogs, which tend to have higher veterinary bills.

- Better Access to Care With insurance, you’re more likely to take your pet to the vet for regular check-ups and treatments. According to the same MarketWatch survey, 83% of pet owners had taken their pets to the vet in the last year, and insured pet parents were less likely to delay necessary care.

- Tailored Plans for Different Needs Many pet insurance providers offer customizable plans based on your pet’s age, breed, and pre-existing conditions. This allows pet parents to choose plans that fit their budget and their pet’s specific health needs. Monthly premiums typically range from $23 to $49 for dogs and $14 to $25 for cats.

- Emotional Relief Many pet owners see their pets as family members, and the emotional toll of not being able to afford care can be devastating. A 2024 MarketWatch survey found that 16% of pet owners had lost a pet because they couldn’t afford the required medical treatment. Insurance offers an emotional safety net, knowing that you can provide the best possible care when it matters most. In addition, some breeds are prone to certain conditions that are much more expensive than average (e.g., dogs with a predilection to disc disease – Dobermans & Dachsunds). Be sure to partner with your veterinarian to determine breed or genetic-based risk assessments.

The Cons of Pet Health Insurance

- Premium Costs Add Up While insurance can save you money in the long run, the upfront costs can be a deterrent for some pet parents. The average cost for a comprehensive plan is around $600 per year for dogs and $300 per year for cats. For pet owners already balancing expenses, this may not seem like the best use of resources.

- Limited Coverage for Pre-existing Conditions One of the biggest drawbacks is that most pet insurance plans do not cover pre-existing conditions. If your pet has a chronic illness, it may be difficult to find a plan that provides adequate coverage. It’s crucial to read the fine print of any policy to understand what is and isn’t covered.

- Reimbursement Model Unlike human health insurance, pet insurance often works on a reimbursement basis. You’ll need to pay the vet upfront and then file a claim to be reimbursed, which can take time. This can still leave you in a difficult financial situation if you don’t have the funds on hand for an emergency.

- Not Always Necessary for All Pets Insurance can be less cost-effective for younger, healthy pets that are less likely to have medical issues. Some pet parents opt to set aside a savings account for vet bills instead of paying monthly premiums. This can be a viable option if your pet is generally healthy and you’re willing to take on the risk of an unexpectedly high bill.

“The decision to get pet insurance ultimately depends on your tolerance for risk and your willingness to manage unexpected expenses,” says Kristen Lynch, Executive Director of NAPHIA. “It’s an investment in your pet’s long-term health.”

The AVMA (American Veterinary Medical Association) has recently been proactive in addressing the importance of pet insurance. They have revised their policy to encourage veterinarians to educate clients about pet insurance, aiming to increase awareness of how it can support veterinary care and help with managing medical costs for pets. The AVMA highlights the significance of having comprehensive coverage, especially given the rising costs of advanced treatments and routine care. The organization also supports the Pet Insurance Model Act, which sets standards for the pet insurance industry to ensure transparency and fairness for pet owners.

For veterinarians, this education effort is seen as an opportunity to discuss financial planning for pet care, helping clients understand the benefits and limitations of pet insurance, such as coverage for preventive care, illness, and accidents.

You can find more detailed information on the AVMA’s website or their dedicated articles about the topic.

Is Pet Insurance Right for You?

Ultimately, whether or not to get pet insurance depends on several factors:

- Your Financial Situation: If you can comfortably set aside savings for potential emergencies, pet insurance may not be essential. However, if a $5,000 vet bill would strain your finances, insurance could be a lifesaver.

- Your Pet’s Age and Breed: Older pets and breeds prone to medical issues, such as large dogs with joint problems, are more likely to benefit from insurance.

- Your Risk Tolerance: Some pet parents prefer the peace of mind that comes with insurance, while others are comfortable taking the financial risk.

Designing the right policy for your situation: While insurance may not cover all routine or wellness visits, it can provide substantial coverage for emergencies, accidents, and chronic illnesses. Pet insurance may offer financial security and peace of mind for owners who want to ensure the best possible care for their pets without worrying about the cost.

Before purchasing a policy, talk with your veterinarian and research various providers to find the coverage that best suits your needs. Your vet and insurance advisor can help you with the right decisions to craft a policy that meet your fur family’s needs:

- Deductibles and Coverage Limits: Make sure to understand the deductible you’ll need to meet before insurance kicks in, as well as any coverage limits.

- Routine Care vs. Emergency Care: Some plans offer wellness coverage for routine checkups, but others focus solely on emergencies. Decide what makes sense based on your pet’s needs.

A Potential Boost from the PAW Act: There’s also exciting news on the horizon! The People and Animals Well-being (PAW) Act, currently under review in Congress, would allow pet parents to use Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) to pay for pet insurance premiums. I was on Capitol Hill with other pet industry professionals for the announcement of this bill by the Human Animal Bond Research Institute (HABRI). If passed, this legislation could provide some serious financial relief and make it easier to keep your furry family members insured and healthy. So, stay tuned—this could be a game changer!

Keep in mind the limitations, exclusions, and the likelihood of increased premiums as your pet ages. Ultimately, pet insurance is a personal decision that requires careful consideration, but for many, it is a valuable investment in their pet’s health and well-being.

It’s easy to think that pet insurance is the magical solution to cover every vet bill but think again! While pet insurance can be a lifesaver when your dog pulls a daredevil stunt or your cat decides to snack on something suspicious, it’s not a catch-all. Just like your own health insurance, pet policies come with fine print and exclusions. The trick is understanding what you’re getting—and where you might still need to pull out your wallet. Here’s a quick rundown to set realistic expectations:

Pet insurance primarily focuses on handling unexpected health expenses due to accidents or illnesses. Most policies cover emergency treatment, diagnostics, and specialized care. Typical inclusions are:

- Injury-related costs (e.g, broken bones, wounds)

- Surgeries (e.g., tumore removals, ligament repairs)

- Chronic condition management (e.g., diabetes, allergies)

- Hospitalizations and emergency visits

- Medications and prescription diets

Even the best plans have exclusions. Standard policies usually don’t cover routine care or elective procedures, so it’s important to understand what’s not included.

The Merits of Wellness Plans:

From my perspective, wellness plans can be a valuable addition because they offer coverage for routine and preventive care that standard insurance policies won’t. They’re ideal for pet parents looking to budget for expected yearly expenses like vaccinations, dental cleanings, and annual health screenings. This proactive approach can help catch health issues early and reduce long-term veterinary costs, ultimately leading to a healthier pet and more predictable spending.

A few examples of what wellness plans typically cover:

- Annual checkups and vaccinations

- Routine dental cleanings

- Microchipping and spaying/neutering

- Preventive treatments (e.g., flea, tick, and heartworm prevention)

While wellness plans add to monthly costs, they provide peace of mind knowing that these essential services are covered. If your goal is to ensure comprehensive care for your pet, adding a wellness plan to your accident and illness coverage is worth considering.

Sources: